De favoriet van de lezers is momenteel uitverkocht.

Parameters

- 692bladzijden

- 25 uur lezen

Meer over het boek

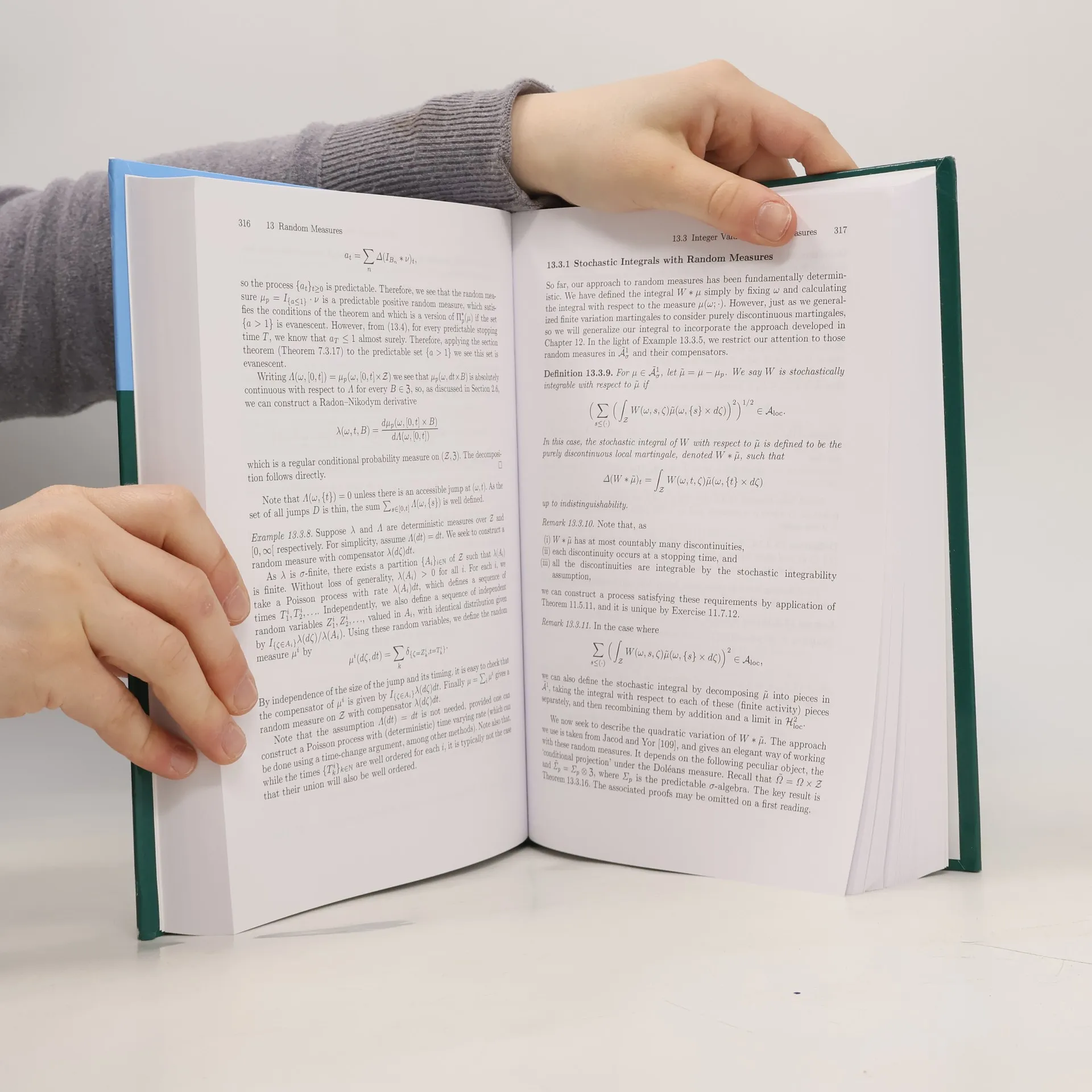

The revised edition offers an in-depth exploration of modern random processes and stochastic integrals, catering to readers familiar with basic analysis. It serves as a comprehensive resource for systems theorists, electronic engineers, and professionals in quantitative finance. Expanding on its predecessor, the text is particularly valuable for research mathematicians and graduate students, as well as quantitative analysts in the finance sector, providing essential insights into contemporary applications.

Een boek kopen

Stochastic Calculus and Applications, Samuel N. Cohen, Robert Elliott

- Taal

- Jaar van publicatie

- 2015

- product-detail.submit-box.info.binding

- (Hardcover)

Zodra we het ontdekt hebben, sturen we een e-mail.

Betaalmethoden

We missen je recensie hier.

- Titel

- Stochastic Calculus and Applications

- Taal

- Engels

- Auteurs

- Samuel N. Cohen, Robert Elliott

- Uitgever

- Springer New York

- Jaar van publicatie

- 2015

- Formaat

- Hardcover

- Aantal pagina's

- 692

- ISBN13

- 9781493928668

- Reeks

- Tags

- Non-fictie, Handel, Business & Management, Technologie & Industrie, Wetenschap en Wiskunde, Wiskunde, Elektronica & Elektrotechniek

- Beoordeling

- 4 van 5

- Aantekening

- The revised edition offers an in-depth exploration of modern random processes and stochastic integrals, catering to readers familiar with basic analysis. It serves as a comprehensive resource for systems theorists, electronic engineers, and professionals in quantitative finance. Expanding on its predecessor, the text is particularly valuable for research mathematicians and graduate students, as well as quantitative analysts in the finance sector, providing essential insights into contemporary applications.